In many parts of India, the dream is straightforward: a safe house on your own land, or a small home in your village where your family can finally stop moving from one temporary arrangement to another. The problem is that finance rarely feels designed for rural life. Income can be seasonal, paperwork can be thin, and the nearest branch may be far away. That’s where a rural housing loan fits in. It is a home loan you take to buy, build, or improve a house in a rural or semi-rural area—typically with flexible tenures and a simpler approach to income assessment.

In 2026, lenders still price loans mainly on your profile and the property. Market data shows home loan rates in India broadly range from about 7% to 12.6% at the start of 2026, depending on lender and borrower risk. Rural borrowers may see a wider spread because property profiles and income patterns vary more than in metro salaried cases. Still, if you prepare properly, you can improve your chances of approval and keep your monthly burden sensible.

What a rural housing loan can be used for

A rural housing loan is typically used for one of these goals:

- Buying a ready-made home in a village or small town

- Building a house on a plot you own

- Buying a plot (where the lender allows it) and constructing later

- Renovation or extension (adding a room, toilet, roof repair, flooring, etc.)

The loan stays secured against the property, and you repay it through EMIs over the agreed tenure.

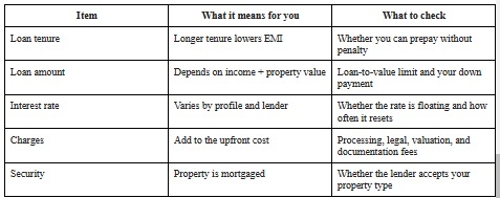

Key features you should look for

Not every lender offers the same experience in smaller towns. While comparing options, check for these features:

Tenure flexibility: Many lenders offer long tenures, sometimes up to 30 years, which keeps EMIs manageable.

Transparent charges: Ask for a full list—processing fee, legal/valuation fees, stamp duty, and any service charges.

Prepayment comfort: If your income is seasonal (harvest, contract cycles), the ability to part-prepay helps a lot.

Documentation practicality: A lender that accepts alternate income proof reduces friction.

,Service reach: Some lenders support collections and documentation through local teams.

If you want a well-known option, Bajaj Housing Finance also operates in many locations and can be part of your comparison set. (Always compare the final offer, not just the headline.)

Eligibility checklist for rural borrowers

Most lenders broadly look at the same basics for a rural housing loan: age, steady income (even if non-salaried), credit behaviour, and property documents.

Standard eligibility conditions

- You are an Indian resident (NRIs rules differ).

- You are usually 21+ at application, and the loan generally finishes before retirement age norms.

- You show a stable earning pattern (salary, business, agriculture-linked income, or mixed income).

- You meet internal credit checks (CIBIL and banking discipline).

If your income comes from a kirana shop, dairy, tailoring, transport, a small workshop, or contracting work, lenders may still consider it, especially when bank inflows and cash flows support the story. In many real cases, borrowers use a co-applicant (spouse/earning family member) to strengthen the file.

Documents required

For a rural housing loan, the exact list can change by lender and property type, but the usual checklist looks like this:

- KYC (any one from each set)

Identity proof: Aadhaar, PAN, Voter ID, Passport, Driving Licence

Address proof: Aadhaar, Voter ID, Driving Licence, Passport, ration card, rent/lease agreement, and utility bills (where applicable)

- Income proof (any combination that fits your profile)

- Salaried: Salary slips, Form 16, bank statements

- Self-employed: ITR (if filed), business proof, GST (if applicable), bank statements, basic financials

- Mixed/informal: Bank statements, cash flow notes, proof of business existence, invoices/receipts where possible

Property papers (most important in rural cases)

Title papers and chain documents

Sale agreement/allotment/builder documents (if any)

Tax paid receipts, encumbrance details (as required)

Approved plan and construction estimate (for construction loans)

If your documents are incomplete, fix that before you apply. Rural files often fail not because of income, but because the property trail is unclear.

Rural housing loan snapshot for 2026

Here’s a clear view of what you should evaluate.

At the start of 2026, market reporting shows housing loan rates across banks and HFCs broadly range from about 7% to 12.6% p.a. Your final number can sit anywhere in that band depending on risk and documents.

Benefits you can realistically expect

A rural housing loan can be genuinely useful when you plan it around your cash flows.

1. Long repayment window

Long tenures spread the burden. That matters if your income is uneven across the year.

2. Better fit for mixed income

Many lenders now look beyond salary slips and focus on banking discipline, inflows, and business continuity.

3. Scope for planned prepayments

If you get yearly bonuses, contract closures, or seasonal surpluses, part-prepayments can cut total interest sharply.

4. Support for improvement and extensions

A rural housing loan is not only for buying; renovation and extension loans can solve real living problems.

If you’re comparing lenders, include Bajaj Housing Finance in your shortlist as well, especially if serviceability and branch/field support matter to you. Always read the final sanction terms carefully; Bajaj Housing Finance rates and approvals can vary by borrower profile and property.

Drawbacks you should not ignore

You should go in with open eyes.

Interest adds up over time: A longer tenure lowers EMI but increases total interest outgo.

It’s a long commitment: Any income disruption can stress your budget if you stretch too much.

Property quality matters: If land title or approvals are messy, lenders may reject or delay the file.

This is why you should keep a buffer of at least 3–6 EMIs before you take the final plunge.

Step-by-step application process

Here is the practical sequence most borrowers follow for a rural housing loan:

1. Fix your budget: Decide your EMI comfort zone and down payment capacity.

2. Check the property papers early: Do not wait for the sanction to find title issues.

3. Apply with a lender: Online or through a branch/field officer.

4. Submit KYC + income proof: Keep it clean and consistent with your bank statements.

5. Valuation + legal checks: The lender verifies market value and legal ownership trail.

6. Sanction letter: Read interest type, reset rules, charges, and conditions.

7. Disbursement: Full disbursement for ready homes; stage-wise for construction.

If you prefer a single lender journey with a wider reach, Bajaj Housing Finance can be evaluated for processing and service experience in your area. Compare it against at least one bank and one other HFC before you decide.

Government support: What you should know

People often mix up “rural housing loans” and rural housing schemes. They are different. A loan is the lender’s money you repay. A government scheme is support, based on eligibility.

For rural households, PMAY-Gramin has provided assistance amounts that differ by terrain (plain vs. hilly/difficult areas), and eligibility depends on government criteria and local verification rather than bank underwriting. If you think you qualify, check your Gram Panchayat and the official PMAY-G channels before committing to a high loan burden.

In conclusion: A quick decision checklist before you sign

- Do you have a clear title and a clean property document chain?

- Can you afford the EMI even in a “thin income” month?

- Did you compare at least two offers and the effective cost (rate + fees)?

- Can you part-prepay without nasty surprises?

- Did you keep a buffer fund?

If you can tick these off, a rural housing loan becomes a tool for stability, not stress. And if you are considering Bajaj Housing Finance – or any other lender, check the final rate offered, the fee sheet, and the service terms, and then decide.

Want to get your story featured as above? Click Here!

Disclaimer: This is a Press Release distributed by HT Syndication. For queries write to contentservices@htdigital.in